Seeking new avenues for yield and portfolio diversification is driving buy-side firms to explore more complex instruments such as mortgage-backed securities (MBS). While once considered a risky investment type in the immediate aftermath of the financial crisis, today MBS are considered a safe and very promising investment for firms looking to maximize their returns.

In a past blog post, The Secret to Success in MBS Modeling, I explained that because MBS are complex instruments, many struggle with modeling them. I also discussed that there is no single gold standard model that should be used for modeling MBS. What’s most important is not the model you pick, but whether you are using the same modeling framework consistently across all securities in your portfolio.

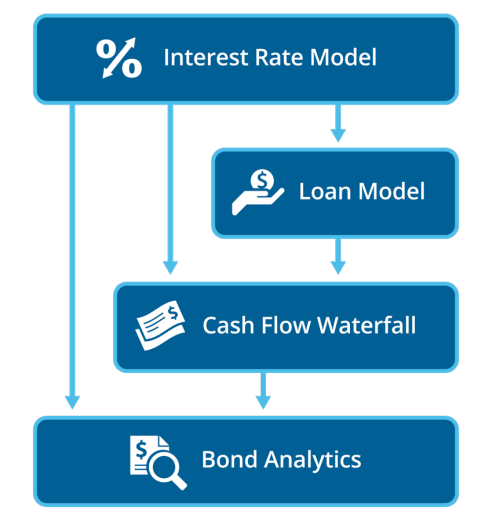

In fact, many firms are finding success using a flexible, modular approach to MBS analytics. To accomplish this, they are designing their MBS analytics framework by first identifying the fundamental elements in their analysis workflow. From there, they use these elements as building blocks that combine to form a complete MBS analytics system. A sample framework might include the following components:

- Interest Rate Model: The interest rate model produces simulated paths of future interest rates. Such a model generally takes inputs such as the current term structure and some model-specific parameters, which are typically determined by calibration to quotes of market instruments.

- Loan Model: The loan model embodies the modeling assumptions for the dynamics of the loans backing an MBS, which include prepayment, defaults and loss severities.

- Cash Flow Waterfall: The complexity of the cash flow waterfall can range from straightforward agency fixed-rate pass-throughs, all the way to collateralized mortgage obligations with multiple tranches that cover the spectrum of payoff types.

- Bond Analytics: Finally, we need analytics capable of performing the desired calculations that inform portfolio management decisions.

MBS Building Blocks

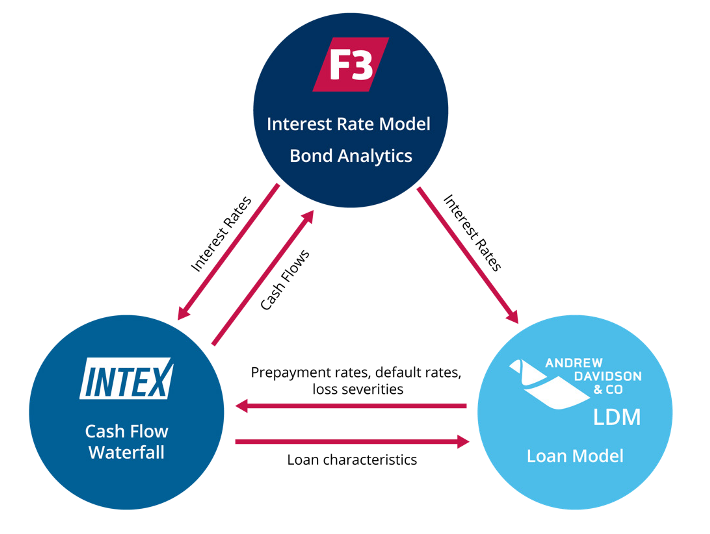

Building on this concept of the modular MBS framework, I’d like to explore a real-life scenario. Depicted in the image below is an example of a complete MBS solution that was implemented according to the paradigm described above. The framework is the result of an integration of three pillars. At the top vertex of the triangle is FINCAD F3, which is our portfolio valuation and risk solution. It plays the role of interest rate model and bond analytics library.

Sample MBS Framework

At the bottom right of the image is the LoanDynamics Model (LDM) by AD&Co. It is a proprietary, commercially available prepayment and credit model for mortgage assets, and is the loan model in our example. At the bottom left is the cash flow waterfall, which in this case is supplied by Intex, a provider that offers comprehensive cash flow modeling coverage for global MBS. The arrows along the edges of the triangle show how different types of information flow among the vertices. You can read our press release for more information on how AD&Co and Intex integrate with FINCAD F3.

The integration shown above achieves a high degree of automation in the MBS analysis workflow. For example, the only information required to specify an MBS is an identifier like a CUSIP. Once the security has been identified, the relevant characteristics of the loans backing the deal are automatically queried from the Intex cash flow waterfall and supplied to the AD&Co LDM to inform the modeling of prepayment and defaults. The challenge of data maintenance has also been made more manageable, in that the Intex cash flow waterfall and the AD&Co loan model will each take care of their own significant data requirements as part of their solutions, out of the box.

The benefits of using a modular MBS framework like that described above are numerous. This MBS framework design is flexible enough to support any kind of MBS analysis that you might want to carry out. Each module in the framework can be swapped out and replaced as desired, without affecting the other parts of the system. This enables you to save time and focus on areas of your business where value creation is greatest.

For more information on MBS modeling, download our eBook: Best Practices in MBS Valuation and Risk