While buy-side technology budgets have leveled out, spending on portfolio risk and analytics platforms (aka RiskTech) is accelerating. In fact, a newly-released Greenwich Associates research report (Developments in Buy-side Risk Technology) found that three out of four investors are evaluating changes to their risk management platforms in the coming year.

Greenwich Associates and FINCAD recently co-hosted a webinar to explore the future of risk technology for the buy-side, and to review the new Greenwich research. In the study, a group of 54 portfolio managers, risk managers, quantitative analysts and traders from asset managers, hedge funds, pension funds, and insurance companies where questioned about their use of risk management technology.

Kevin McPartland of Greenwich Associates, alongside FINCAD’s James Church and Dan Connell, also of Greenwich, had a lively discussion about the study findings. Kevin explained that there is clearly a surge in institutional investors looking to upgrade their risk systems. And in actuality, this isn’t the first time that spending on RiskTech has spiked.

Spending also surged just following the financial crisis. Market participants rushed to understand what had happened. They then put mechanisms in place to prevent being caught off guard again, and to comply with the onslaught of new regulations. These expenditures in 2008 were defensive. But today the story is different as institutional investors take a more offensive approach to risk.

Why is RiskTech growing in importance?

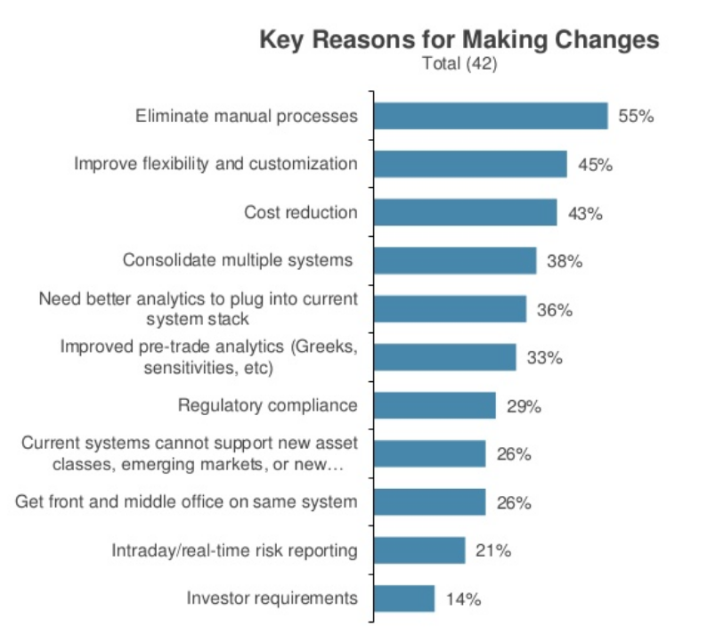

One big reason is the need for automation (as reported by 55% of Greenwich’s surveyed respondents). The more efficient trading desks can be and the least they need to do manually, the better. Tasks like running batch processes overnight are really not feasible anymore from an operational standpoint.

Customization (45%) is another area for improvement. Firms want the flexibility to program and create models in whatever language they choose and/or are comfortable with. The level of customization we’re seeing today is something that did not exist in the past. But there are a select few risk technology vendors that are now offering it.

A third area buy-side firms are focused on with respect to risk systems is cost reduction (43%). Building and maintaining software in-house can be expensive (as many of us well know). Even new methods of deploying third-party software such as using the cloud to run analytics can run up your costs.

So what are the biggest shortcomings of firms’ current risk systems?

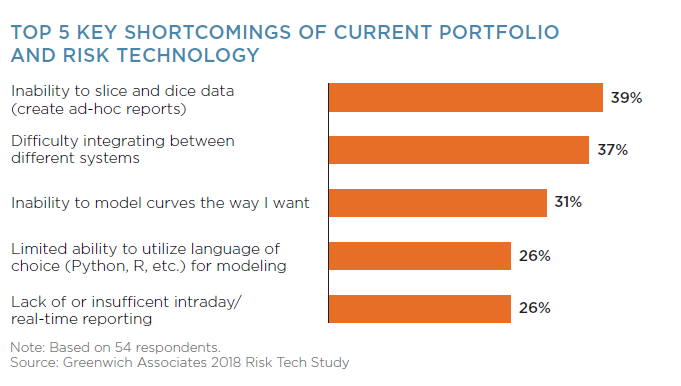

According to the research, the top three included an inability to slice and dice data (39%), difficulty integrating between different systems (37%) and an inability to model curves according to a user’s needs (31%). Interestingly, all three of these shortcomings are rooted in a lack of flexibility—the inability to create ad-hoc reports, choose between Python and R, model custom curves, and the limited programming language choices. That lack of flexibility matters because it limits the ability to enter new markets, utilize new products and trade with new counterparties—all revenue-generating and/or cost-saving activities.

James described that many of the trends reflected in the research ring true with clients he is regularly in contact with. “It’s getting harder to make returns, there is a downward pressure on fees, and increasing competition among other serious factors. These dynamics are all driving buy-side firms to make changes to their risk technology,” he commented.

James described that many of the trends reflected in the research ring true with clients he is regularly in contact with. “It’s getting harder to make returns, there is a downward pressure on fees, and increasing competition among other serious factors. These dynamics are all driving buy-side firms to make changes to their risk technology,” he commented.

James went on to explain how he also talks to many asset managers looking to get into new asset classes to find yield. They are trying to figure out how to do this in terms of learning what technology changes they need to make to enable entry to new, esoteric asset classes. For a particular client James recalled, their technology was built a long time ago and simply did not have the ability to expand. “This is one firm, but the story is a common one for many buy-side firms these days,” he remarked.

James also spoke to one firm that felt like they were operating in the Stone Age with rampant manual processes and spreadsheet usage. They wanted to take control of their business back and put into place a technology that would centralize their workflow and make it more efficient. And perhaps, along the way, this client also wanted to reduce the number of systems they were working with.

What do some of these risk system upgrades look like?

For the most part, firms are not looking to do big rip and replace overhauls because of the magnitude and risk involved in that type of project. So, if firms can find technology that enables them to achieve their goals by integrating with the technology they already have in place that is most desirable. They can make small changes and then expand the footprint of their technology from there. For example, one firm’s primary focus might be adding a new asset class. Once they have completed this smaller task successfully, they can turn their attention to using the technology to enhance or improve other areas of the business at their own pace.

To hear more of the discussion, view our on-demand webinar: The State of RiskTech for Buy-side Investment Managers

Read the Greenwich research report: Developments in Buy-side Risk Technology